The Offset Mortgage is growing in popularity as savers continue to struggle to earn a good interest rate on their savings. Interest rates on savings remain at around 1% which means homeowners could benefit by combining their savings and mortgage balances. Offset Mortgages currently only account for 10% of the UK mortgage market. Are borrowers missing out?

Offset mortgages connect your savings or current account and your mortgage. You will earn no interest on your savings and in return, you will pay a lower interest rate on the mortgage. You keep your savings in the offset account with the amount being saved is deducted from the balance of your mortgage. The interest you pay is only on the difference between the savings amount and the mortgage balance which means in the unlikely event you had savings equal to your mortgage amount, you wouldn't pay any interest at all.

What is an Offset Mortgage?

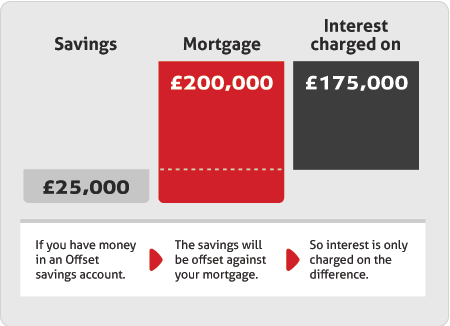

An offset mortgage product links your savings account - and sometimes your current account too - to your mortgage. You are required to hold all of these with the same bank or building society and rather than earn interest on your savings (and possibly, current account balance) you pay a correspondingly smaller amount of mortgage interest. You sacrifice the interest that would be earned on your savings in return for smaller monthly mortgage payments. As an example, if you have savings of £25,000 and a mortgage of £200,000, you would pay mortgage interest on £175,000 only (and receive nothing on your savings.) This allows you to reduce the amount of interest you will pay on your mortgage overall, and allows you to pay it off in less time.

This type of mortgage is both flexible and tax efficient. While many standard mortgages will allow you to make overpayments, once you've paid the money you can't get it back. With Offset Mortgages, you retain access to your entire savings balance in case you need to dip into it - effectively allowing you to borrow at the main mortgage rate, against your property. They are also very tax efficient, as most non-ISA savings accounts are subject to income tax on interest earned. Offset Mortgages are suitable for most borrowers, especially people with a lot of money saved or annual bonus scheme.

The BOE Base Rate remains at a historical low and is likely to do so for some time. This means that interest rates on even the very best savings accounts are sitting at 1% or less. With mortgage interest rates far above this (around 3%) it makes a lot of sense to opt for an offset mortgage at this time.

Comparing The Market

You will find that offset mortgages also come in a range of types, including variable and fixed rates. They tend to require a minimum deposit of 25% and will often require a higher proof of earning. Look for those with the lowest interest rates and fees, and compare the overall APR. Look for products which offer additional benefits, such as the chance to link your current account and ISA too, so that your money is working as hard as possible. Remember that your offset mortgage means your mortgage and savings accounts must be with the same bank or building society.